The first “bad policy” from the Fiscalbridge library was a Variable Universal policy and here we are going to look at a Universal. I call these kinds of policies “cross-breeds” because there are a few differences but at the end of the day, they are not performing better than each other.

Again, I have removed the name of the company as I don’t feel the company is important. It’s the type of policy and how it’s being sold that is important. These policies can work if you fund them correctly and hope and pray your return is what they (the agent or company) say it will be.

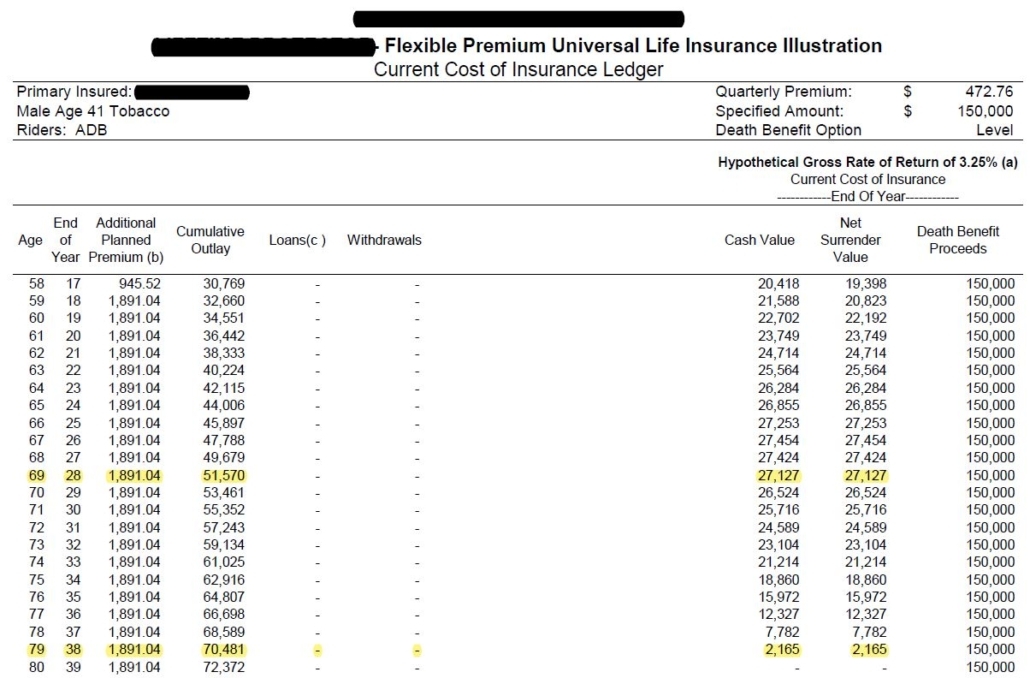

What you are seeing here (sorry it’s a little small) is $1,801.04 a year premium. He has paid a premium on this policy for 16 years already and should have an established policy. Yet we look down to year 28 when the insured is 69 years old and see his cash value starts to decrease every year, even though he is paying his premium. Continuing to follow those numbers we see by age 80 his policy terminated due to no cash value. Unless of course, he wanted to pay unbelievably high premiums to keep it in place.

This is based on a 3.25% rate of return. That is not even that high of a ROR, yet the policy is not going to last. This story does not end well. This insured is no longer insurable as he has an aneurysm by his heart. On top of that, he does not have enough money to start another whole life policy which means death benefit is very very important to his family. Unlike most people who call me and want cash value, these people wanted both. I can’t give them either!

This story does not end well. This insured is no longer insurable as he has an aneurysm by his heart. On top of that, he does not have enough money to start another whole life policy which means death benefit is very very important to his family. Unlike most people who call me and want cash value, these people wanted both. I can’t give them either!

Their agent did not look long term or they would have seen this themselves. This kind of stuff rips me apart. I can’t save the policy nor can I help them save the farm they are operating. The only thing I could tell them was he has to pass before 80 or there will be nothing there.

No one time their death and these policies are putting time frames on our lives.

Please watch what you are buying. If your agent is not looking long term you need to be. It is beyond me how agents don’t look at those dashes and show their client that the policy may terminate at that time. Look at your policy are there dashes or zero’s before the illustration stops?

If you have questions on your policies, whether variable universal or whole life, please call me or email them to me so I can take a look. If they are right I’ll tell you to keep it. I am not here looking to replace people’s policies, I am here looking to educate and be sure you have something when you were supposed to have it.

0 Comments