Over the years, I’ve accumulated illustrations and a handful of insurance policies from my clients, people who have attended the Secure Wealth Builders Conference, and others who end up in my office because they didn’t see the light at the end of the tunnel. The information in this post is meant to educate and create awareness for those looking for answers and those who want to make sure their insurance policy is set up to benefit them the most.

If you’ve read any of my books or blogs, you have heard me talk about fees and charges inside policies that are not whole life policies. Other permanent products have these and on most account agents are sharing this information with you.

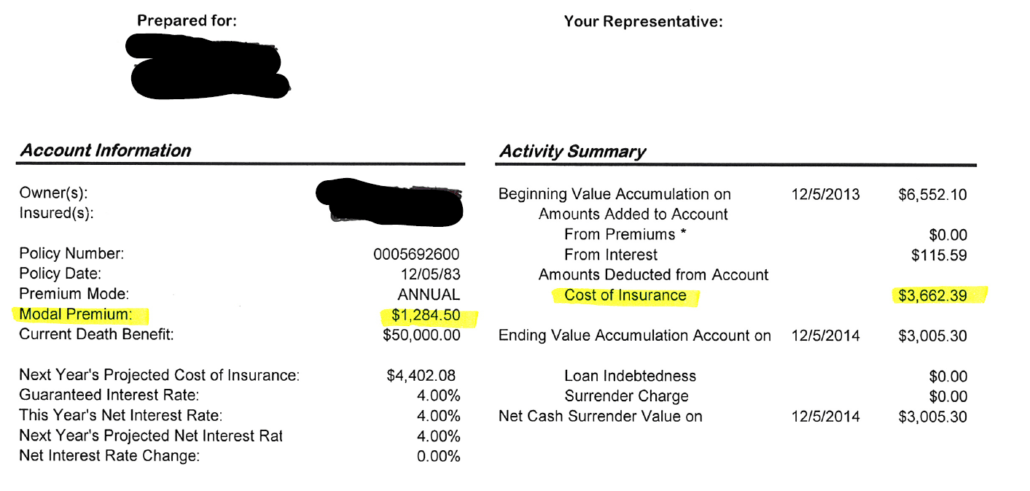

Here is one of those charges: Cost of Insurance (COI) is the expense factor which is the amount the company adds to the cost of the policy to cover operating costs of selling insurance, investing the premiums, and paying claims.

Every company has these COI charges but how they are handled is not the same for every company. Mutual companies take these charges from your dividend before they give it to you. Meaning the dividend you get is after all these are paid, yet you still get a dividend! In a policy like you see below, that does not happen.

What you are looking at here is a variable universal policy with a non-mutual company. First things first, there are no dividends being given to policy owners so there is no place to get this money from beside you as the policy owner. Second, in these companies have recently gotten in trouble for astronomical increasing costs of COI’s. As you can see here, the COI charge was $3,662.39 and the projected amount for next year is $4,402.08. That is an increase of $740 in one year!

These COI’s are increasing rapidly with some companies because they have over projected the rates of return on these policies. The difference has to be made up somewhere and that is being passed off to you.

You can clearly see this insured has a yearly premium of $1,284.50 and his COI is MORE than his premium! What are they doing to cover the difference? They are taking money from his cash value to supplement.

Look at is cash value, there is only $3005.30 left, this policy will collapse on him the next year unless he pays in more than the premium due. His premium plus his cash value does not even cover the projected COI for next year.

Sadly, this policy was issued in 1983, it was 2015 when he brought this to me. He was sold this policy that he would have money for retirement and make great rates of return. He is now around 83 years old and he has NOTHING!

When I warn about these policies it is not so I can sell more insurance, it is so you as the consumer are educated enough to make the right decision. Whole life is not the same as these other permanent products. Whole life with a mutual company is not the same as whole life with a non-mutual company. Dividends and guarantees are important.

This story is just one that I’ve heard over my career.

If you see anything here that you have questions about or if it sounds familiar, please contact your agent.

0 Comments